LLC Business Bank Accounts

One of the main reasons for forming your LLC was the protection it provides. By separating your personal assets from your business assets you protect each from being affected by the other. This is known as a “corporate wall”. You want to do everything you can to prevent something (read; lawsuit) from piercing that corporate wall.

Remember, your LLC is a separate entity. Think of it as being another person, one that makes its own money, has its own bank account, and has its own income, expenses, and debt. This is important in the eyes of the courts. Without a separate bank account for your LLC you will be “commingling funds” or mixing your personal money with that of your business. If you were to do this a court may determine that your corporate wall has been pierced and make you personally liable for your business’s debts and obligations. If that happens all the steps we have completed up to this point become moot. In addition to losing your LLC protections you have now subjected yourself to different tax laws, not to mention possible fines and/or charges related to how you have been operating your business.

However, there is no set rule requiring that you do so. Sound odd? It is.

IRS regulations simply require businesses to keep good records of their income and expenses. To accomplish this the IRS believes a business should maintain a deposit account in the business name into which all income is deposited. The downside of there being no set rule on this from the IRS is that you are fully free to make your own mistakes and ruin your business.

Note: This doesn’t mean you can’t move money between your personal account and your business account; you can. However, some banks require that you do so in person at a local branch. This is the fallout from several cases where large corporations (Enron) and large hedge fund operators (Madoff) were allowed to do so with no oversite, resulting in massive fraud. To do this form of transfer today requires a special corporate resolution. Even then, it is ill-advised. As of this writing there are some banks that are once again allowing this. That may change with new political leadership.

Opening a business bank account for your LLC makes life easier for you, your accountant, and the IRS. It also helps you maintain the personal liability protection your LLC brings.

Other reasons to have an LLC bank account are:

It’s easier to keep accurate financial records

It’s easier to calculate and pay taxes

It reduces red flags that might trigger an audit

it’s easier to track/deduct business expenses

it offers a degree of professionalism and credibility (using business checks instead of personal checks)

Online Business Banking Options for Indie Authors

Traditional brick-and-mortar banks are not the only option. Several digital-first business banking services have become popular with indie authors and small publishers, particularly for their fee structures and ease of remote account management:

Mercury — A technology company offering free business banking (no monthly fees, no minimum balance requirements). Popular with online businesses and solo entrepreneurs. Fully online — no branch visits required. FDIC-insured through banking partners.

Relay — Designed for small businesses and freelancers. Offers up to 20 individual checking accounts (useful for authors who separate income streams by pen name or series) and automated savings rules. No monthly fees. FDIC-insured.

Novo — Small business banking with no hidden fees, reserve features for setting aside tax money, and integrations with common small business tools. FDIC-insured.

Digital banking services handle most author business banking needs efficiently and at lower cost than traditional banks. The primary limitation is the absence of physical branches — if your business regularly handles cash deposits, a traditional bank or credit union remains necessary. For publishing businesses where income arrives as electronic royalty payments from KDP, IngramSpark, and similar platforms, digital banking is often the better fit.

Should I use the bank I have now?

You may be tempted to simply open your new business account at the local bank where you have your personal accounts. You can, but it helps to do a little research first. Your friendly neighborhood bank may be fine for your current needs, but they may be lacking what your business needs. It's advised that you visit a few and talk to the representative who handles business accounts before deciding on which one to go with.

You should ask about the following:

- What are the required documents? Get a detailed list of every document the bank requires in order for you to open an account.

- What are the minimum monthly balance requirements?

- What is the fee if that balance should drop below the minimum? Is this negotiable? Does dropping below the MMB alter the agreement in any way?

- What are the fees?

WARNING: When you ask about fees you want to know about ALL of them. The bank should provide you with a printed list of their fees. Be sure to go over this in detail with the representative as the majority of the fees involved will have vague names and/or definitions at best and one fee may be applicable to several areas. Hidden or ill-defined bank fees have become a huge problem for the consumer in the last decade, and every businessman must do their due diligence to ensure that the bank they are using is not charging them for services they don’t want or need.

How much is needed for the initial deposit?

This is usually negotiable. You’ll want to inquire whether the initial deposit needs to match the Operating Agreement.

Do all LLC members need to be present?

This can be a deal-breaker in today’s world of on-line startups. An LLC may have members located in several states or even several countries. If the bank cannot accommodate this structure it’s a sign that they are behind the times and perhaps not the right fit for your company.

When can the bank alter the agreement and how?

The bank may try to reserve the right to lower your LLC’s credit card limit, freeze your line-of-credit, or even alter the percentage rate attached to your accounts, if you should miss a payment, not keep a minimum balance, or really any excuse they can come up with. Be aware of any clause that speaks to this.

Can the bank wire money? How long does it take and what are the fees?

Most banks can wire money, but the fee is often higher than what you do thought online banking services like Paypal or Remitly. Its best to research wire transfer options before you create a business bank account.

TIP: Be wary of any promotions or incentives the bank offers for opening a new business account. The majority of them are temporary and designed to secure the bank another ongoing monthly fee. Likewise with packages with names attached to them. The “Platinum” package is usually loaded with things your business will never need and comes with higher fees.

What do you really need?

At a minimum, you want to come out of your bank with the following:

- A checking account in the name of your LLC

- A Debit/Credit card. One with the lowest rate possible, and a limit that can finance your business for at least three months. If each member needs a card you may need a combination of the two. But remember, every card comes with an additional fee. It's recommended that each member receive a debit card that will handle whatever business expenses they need to do their job, and the LLC’s manager hold the company credit card to handle capital expenditures.

- Checks. Ask them to start the numbers at 1,000. You don’t need the BIG checkbook, a standard one is fine. Have them list both the LLC’s name and the DBA name on your checks.

Anything more than this is unnecessary. You may get a hard sell to utilize one of the banks “introductory packages”, but chances are it’s full of stuff you will ever need and you’ll pay too much in fees. Stick to the basics, you can always upgrade later.

What the bank will need

You’ll need the following items to open your LLC’s business bank account:

1. Articles of Organization (or equivalent)

This refers to your LLC’s approved (stamped) Articles of Organization, which may be labeled something different in your state (Certificate of Formation or Certificate of Organization).

2. Two forms of Identification

One of these needs to be government-issued (such as a driver’s license or passport). Banks are being more careful about identity theft. They may ask you to produce something that is not normally carried in a wallet or purse. This might be your vehicle registration, voter’s registration, or a utility bill (the utility bill will also serve to confirm your address).

3. EIN Confirmation Letter or EIN Verification Letter.

Most banks will not open a business account without an EIN number. There are two forms that they will accept: EIN Confirmation Letter (form 575 CP) and EIN Verification Letter (form 147C). A copy is usually enough but your bank may wish to see the original.

TIP: If you can’t find your EIN letter you can call the IRS and get a 147C EIN Confirmation Letter faxed to you or the bank. They will usually fax it to you while you’re on the phone.

4. Operating Agreement and Additional Forms

Most banks don’t need a copy of your Operating Agreement or your Welcome/Approval Letter (if you received one), but some banks may require it. We recommend bringing all of your LLC documentation just to be safe. Not only does this save you a trip home to fetch what’s needed, but it keeps the file all together.

5. Declaration of Beneficial Ownership

This is a form that will be provided by the bank. It’s simply a document that discloses who the LLC owners are. Every bank has their own DBO form.

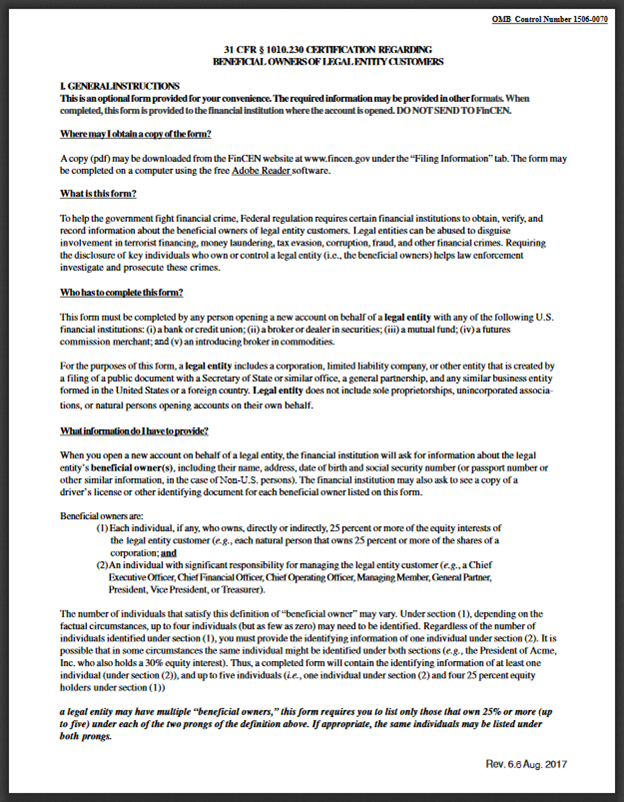

This document relates to the Beneficial Ownership Rule and the LLC Bank Accounts Rule (CDD Rule).

Banks are required by law to verify the identity of the individuals who own or control LLCs when opening bank accounts. This includes LLCs owned by US citizens, US residents, non-US citizens, and non-US residents.

This is all in an attempt to combat fraud.

The actual CDD Rule (Customer Due Diligence Requirements for Financial Institutions) documentation covering this is over sixty pages long. We’ll spare you the legalese and break it down to the five main responsibilities that banks and financial institutions are required to adhere to:

- Identify and verify the identity of their customers

- Identify and verify the identity of the Beneficial Owners of companies who are opening accounts

- Understand the nature and purpose of customer relationships to develop customer risk profiles

- Conduct ongoing monitoring to identify and report suspicious transactions

- Maintain and update customer information

All Beneficial Owners (members) of the LLC need to be reported (and their identities verified) when opening up an LLC bank account. It also doesn’t matter if the LLC owners are US citizens, US residents, non-US citizens, non-US residents, or foreign nationals. The type of taxation the LLC management has selected with the IRS has no affect in regard to the beneficial ownership requirements; all LLCs are affected.

This is not a place where you want to leave out a name.

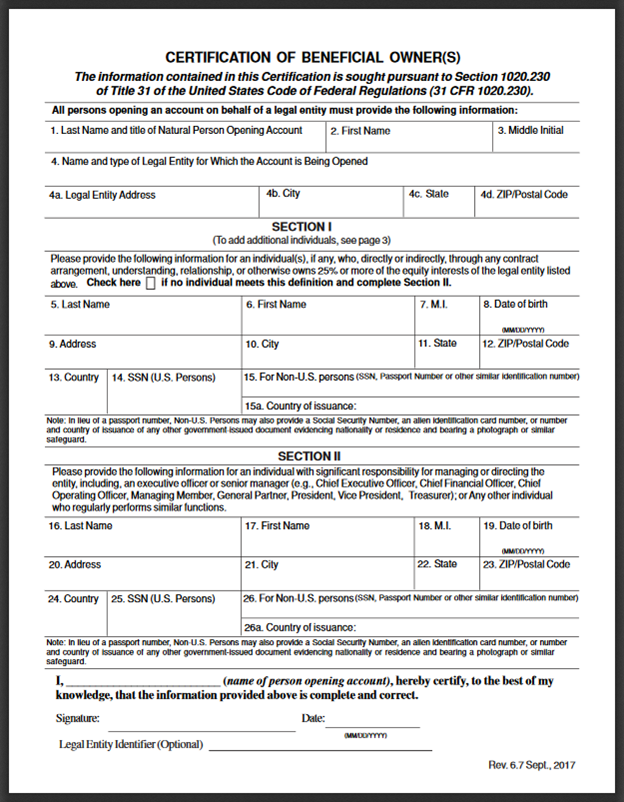

What information is required:

In addition to the LLC’s name, address, and EIN Number, the Beneficial Ownership forms ask for each members:

- name

- date of birth

- a government identification number (such as your Social Security Number)

- current physical residential address or business address

Other possible forms of identification that may be accepted by the bank are:

- state-issued ID with a photograph

- other US government-issued IDs with a photograph

- US government-issued ID with a photograph

- US passport

- Non-resident alien card with a photograph and identification number

If you are a non-US resident or non-US citizen (“foreign national”) and you don’t have a Social Security Number, the bank will ask for the following:

- passport number

- Individual Taxpayer Identification Number (if you have a US tax filing obligation)

- foreign driver’s license number*

*If you’re a foreign national, the bank may or may not accept your foreign driver’s license number. This isn’t specified in the new laws, so it’s up to the bank and their own internal policies. Each bank has their own policies, so it’s best to call ahead to make sure you are bringing the correct documentation.

Although this is a government requirement, and they provide a standardized form, the government does not require the banks to use that standardized form. Each of them have their own.

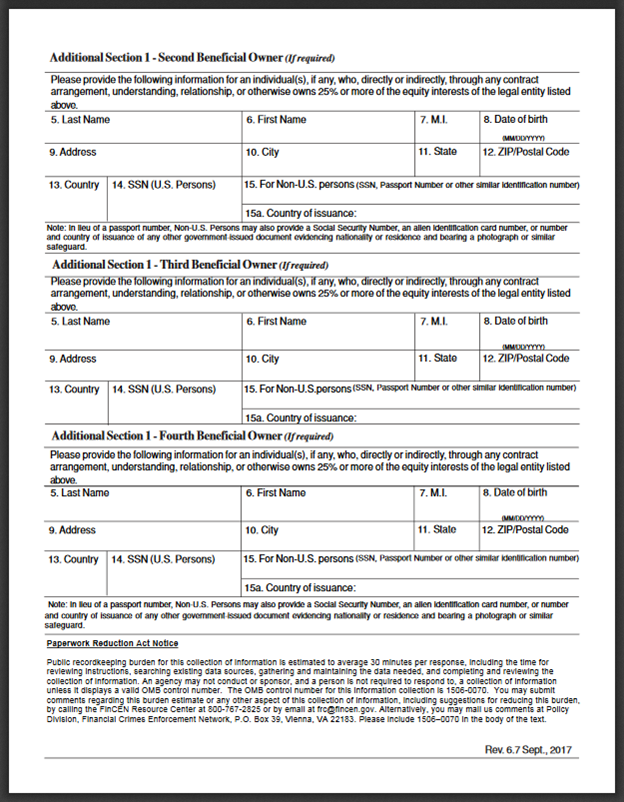

The government’s standardized form is available through FinCEN (Financial Crimes Enforcement Network) . We’ve included a copy below. Your banks should be similar.

![]()

DBA?

The bank may ask for your DBA (Doing Business As) documentation. This is unnecessary as everything you and your bank will be doing will fall under business and should not be using your DBA name. You’ll need to tell the person you are dealing with that you want the full name of your LLC (with the LLC on the end) on every document. If they insist that you produce your DBA document, for the checks for instance, it may be a red flag that you are dealing with a bank that is not that familiar with LLC’s and how they work.

TIP: If you wish, the bank can place both your LLC’s business name AND its DBA name on the checks they will provide you.

If your LLC needs to operate under a name different than the one you registered with the state, and you have a DBA with you, it doesn’t hurt to provide it, as long as you ensure that the banks paperwork utilizes the correct title for your LLC.

Signatories

If your business is a partnership, limited liability company, or corporation, you should have designated signatories for the business account. If your banking institution allows the cashing of checks written out to the business, only the signatories will have the ability to do so.

Each signatory must sign a signature card that is kept on file at the bank.

ScribeCount Author OS — Connecting Your Business Bank Account

Once your LLC's business bank account is open, connect your publishing platform accounts to ScribeCount with your new business bank details. Royalty payments from KDP, IngramSpark, Kobo, Apple Books, and all connected platforms will flow into your business account — the same account your ScribeCount Sales Dashboard monitors. This creates the clean financial separation that protects your corporate wall: royalties go to the LLC's account, ScribeCount tracks the income, your bookkeeping software records the transactions, and your accountant has a complete picture of your publishing company's finances. The Sales Dashboard's Historical view shows your LLC's royalty income over time — the financial record that supports your business banking relationship, your tax filings, and any future financing or partnership discussions.

Conclusion

Your LLC's business bank account is the cornerstone of the corporate wall that protects your personal assets. Without it, the legal separation your LLC creates is at risk of being invalidated by a court that views commingled funds as evidence that the LLC is not genuinely a separate entity.

Open the account as soon as your EIN arrives. Use it for every business transaction. Direct all royalty payments into it. Pay all business expenses from it. And keep your personal money completely out of it.

That discipline — maintaining the financial separation — is what makes your LLC's liability protection real. The paperwork creates the wall; the bank account maintains it.

- Randall